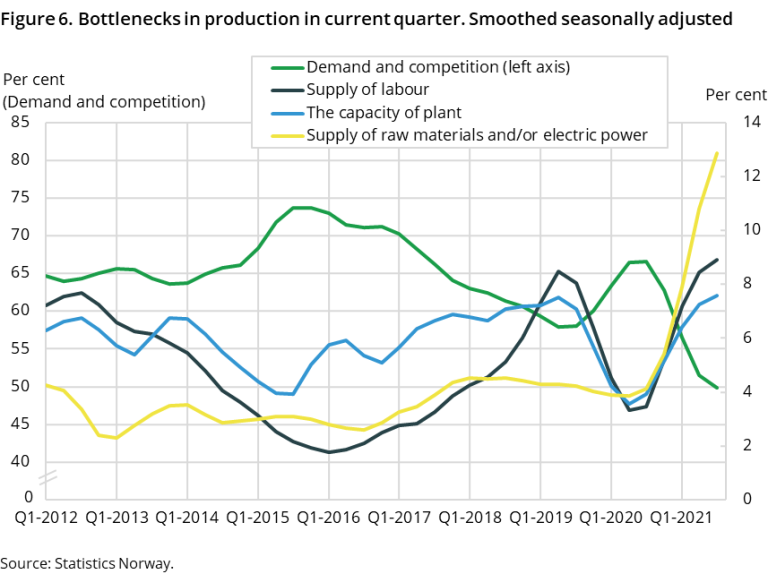

The business tendency survey for the 3rd quarter of 2021 still shows growth in total output compared to the 2nd quarter. The producers of Covers industries such as wood and wood products, paper and paper products, basic chemicals and basic metals. Often referred to as traditional export industries. and Covers industries such as food products and beverages, printing and reproduction, pharmaceuticals and furniture. are experiencing a clear increase in production. Growth among producers of Covers industries such as machinery and equipment, ships, boats and oil platforms, repair and installation. Often referred to as the engineering industry. is more moderate but is positive now for the second quarter in a row after reporting declining production throughout the pandemic. There are still some of the industrial leaders who report that production in the 3rd quarter has been limited by corona- related factors such as access to labour and lack of access to raw materials and other input factors (see figure 6). Lack of raw materials and input factors can be linked to logistics challenges in the world market and production limitations on certain input factors that are imported.

Industrial leaders report growth in total industrial employment in the 3rd quarter compared with the 2nd quarter, and it is especially among producers of consumer goods that increased employment is reported.

High demand and strong price growth

The total stock of orders in manufacturing shows a clear growth in the 3rd quarter. Producers of consumer goods and intermediate goods have a marked increase in stock of orders in the 3rd quarter, while the producers of capital goods are somewhat lower, but clearly growth. The industrial leaders also report clear growth in new orders for the domestic market and the export market. Growth in new orders is reported in both markets for all types of goods. Growth is lowest in the domestic market for producers of capital goods. Here the increase is dampened by unchanged new orders in the machine repair and installation manufacturing.

Industrial managers are reporting significant growth in the prices, both in domestic and export market for overall manufacturing in the 3rd quarter. Price growth is reported for all types of goods in both markets. For producers of intermediate goods, the growth in prices is particularly strong.

As of this survey, two new indicators are published (see box at the bottom of the article) where the development in the companies' The development in the prices that the company pays for the goods and services that are included in the production (product input), and on the prices of production equipment and facilities used in the production process. and The development in the profitability of the company's sales of goods or services. Profitability means the change in the difference between current operating expenses and current operating revenues. is measured. Industrial managers report strong and increasing growth in cost prices, while the profitability is declining in the 3rd quarter.

Positive expectations for the four quarter of 2021

The general outlook for the 4th quarter of 2021 is clearly positive, but the proportion with an optimistic view for the coming quarter is somehow lower than in the previous survey. Although producers of all goods types have positive expectations, it is producers of intermediate goods who have the most optimistic view related to the coming quarter. The industrial managers further report that the total production volume is expected to grow during the 4th quarter compared with the 3rd quarter. Employment growth is also expected in the coming quarter. It is reported that new orders from both the domestic and export markets will increase, and further growth in the total stock order is also expected. The strength of the expected growth for the various indicators is not the same for the different good types. Generally, the strongest growth is expected for producers of intermediate goods and capital goods, while the expected growth is somehow weaker for producers of consumer goods.

It is reported that adopted investment plans are marginally adjusted upwards somewhat for manufacturing. As of, this survey a new statistics table (see box at the bottom of the article) is introduced, it shows the development in which factors the managers state as limiting the investments. In recent quarters, a lower proportion of industrial managers state that expected developments in demand limit the investments. At the same time, an increasing proportion of industrial managers state that the The prices of the investment goods (production equipment and facilities used in the production process) that the company purchases are so high that it limits the implementation of planned investments. constitute a limiting factor in the investments.

The industrial confidence indicator indicates further growth

This is the average of the responses (balances) to the questions on expected volume of production, total stock of orders and inventories of own products for sale (the latter with an inverted sign). See Definitions in ‘About the statistics’ for further details. in the 3rd quarter was 8.8 (Figures that are adjusted for calendar effects and seasonal variation. Such adjustment gives a more accurate picture of the underlying trend in the time series and makes it easier to compare the results of subsequent quarters. which is somewhat lower than in the previous quarter. The indicator is still well above the historical average of 3.1 and this indicates growth in production volume for the four quarter of 2021.

The industrial confidence indicator is clear positive for all the producers of type goods. Compared with the previous survey, the level of the indicator is now more even between the different good types. The level of the indicator has increased markedly for capital goods, while the level is declining, especially for intermediate goods, as well for consumer goods.

Values above zero indicate that total output will grow in the forthcoming quarter, while values below zero indicate that total output will fall. International comparisons of the industrial confidence indicator are available from Eurostat (EU), The Swedish National Institute of Economic Research and Statistics Denmark.

Access to raw materials limits production

Compared with the previous survey, there are a higher proportion of industry leaders who highlight that the lack of qualified labor and supply of raw materials and/or electric power are factors that contributed to limiting production in the 3rd quarter of 2021. At the same time, a lower proportion of industry leaders point out that weak demand and strong competition have limited production. The sum of percentages for those who have reported that lack of qualified labour and raw materials/electric power limits production, plus the percentage of establishments with capacity utilisation above 95 per cent. has risen sharply in recent quarters and is now at its highest level since the 3rd quarter of 2008.

The average How much of the available production capacity is utilised. A high capacity utilisation means that it is difficult to produce more without investing, while a low capacity utilisation means having capacity that is not being used. for Norwegian manufacturing was calculated to 80.0 per cent at the end of the 3rd quarter of 2021. The utilization rate is at about the same level as at the end of the 2nd quarter, and it is now equal to the historical average of 80.0 per cent. International comparisons of average capacity utilisation are available from Eurostat (EU).

Timelines

The survey data was collected in the period from 9 September to 20 October 2021.

As of this publication, new indicators are introduced in the statistics. The indicator «Cost prices» and «Profitability» for actual and expected changes in the next quarter are published in the table «08264: Business tendency survey. Tendencies» Cost prices measure the development in the prices that the company pays for the goods and services that are included in the production of the final item (raw material). As well as on the prices of the capital goods (production equipment and facilities used in the production process) that the company purchases or, in those cases where another part is responsible for the entire investment project, the price of the investment delivery. Profitability measures the development in the profitability of the company's sales of goods or services. Profitability means the change in the difference between current operating expenses and current operating revenues. In this case, it is not considered factors that affect the company's profits that are not directly linked to the company's main activity (eg. sales of electricity). In addition, a new statistics bank table is published which shows reasons that limit the company's investment activity: «12786: Business tendency survey. Limiting factors for investments». For "Limiting factors for investments", business leaders are asked to choose the most important reasons that limit new investments (several answers possible). If they have not planned investments, they can use the option «No special». The reasons that are measured are these: «Access to credit» if they plan to invest in new real capital, but have problems establishing enough financing. «Expected development in demand» if they expect lower demand and for that reason it is risky to invest in new capacity. The alternatives for investment costs are used if it is considered that «Prices for Capital Good» and /or «Financing cost» are so high that it limits the implementation of planned investments. «Governmental requirement» if they conclude that public requirements related to an investment (for example environmental requirements) are so high that planned investments are limited. «Access to governmental subsidy» if the planned investments are limited by rejection of an application for public grants or that the grants are too low. «Available production capacity» if at the end of the quarter they have spare production capacity and for that reason do not wish to carry out planned investments at the present time. Companies that have other limiting factors than those specified in the form, use the option «Other factors» where the business leaders can specify what these factors are.